I’ve always loved the energy of a New Year. It’s alive with intentions and goals and the buzz of a fresh start. This New Year feels even more special because it’s the start of a new decade too. With that in mind, do you know where you want to be in ten years? What do you think 2030 will see you doing?

I spent years dreaming of writing full-time but it wasn’t until I developed a money mindset that the dream of quitting my day job became a reality. This post outlines some of the tips and tricks I used to set myself up, which I hope will help you move into the next decade able to make your dreams a reality too.

Tip 1: Know What You Need

Before you can embark on quitting your job to write full-time you need to know one fundamental figure:

How much money do you need each month in order to survive?

I get asked this question a lot, but no one other than you can answer it. Depending on the cost of living where you are, the amount of bills you have and the amount of debt, that figure will be different for everyone.

Action: create a spreadsheet with your incomings and outgoings.

If you don’t want to create one, head to Google—there are plenty of budget templates available there.

If you do create one, include everything that costs you money. For example:

Utility bills, local taxes, food, insurances, TV licences, Netflix or other subscriptions, internet, sports memberships, childcare, school fees etc.

You should also include potential spending. For example, I go to the local coffee shop once a week to write so I know I need $20 a month to cover that. I also spread the cost of Christmas and summer holidays out over the year by saving each month, so I include that figure too. And, I may or may not give myself a monthly book-buying budget because, you know… we’re all book addicts here.

Essentially, anything that will cost you money needs to go on the list. Once you’ve got your list, tot it up and see what the monthly figure is. That is the minimum amount of money you need to earn regularly from your writing business before you leave your job.

Tip 2: Lose the Debt

A controversial one, I know. But, the fastest way to leave your job is to need as little as money as possible. The more money you have to earn, the harder it is to reach that figure—especially as a new business owner. Most businesses don’t earn a good profit for the first 2-3 years.

If your monthly bills (including debt) total $3000 a month, that’s a lot harder to earn than if you’ve paid off all your debt and reduced your outgoings and as a result only need $1500 a month.

Before I quit my job, I paid off £40,000 in student and car loans and fertility treatments. It meant I needed £800 less each month and that made my monthly figure far easier to reach.

No one’s saying you’re only going to earn $1500 a month from your business forever, but if you want to quit, then the lower the ‘must-earn’ value is, the easier it is to achieve.

Tip 3: Have Savings

I know it’s boring and no one wants to hear it. But trust me, every business will have cash flow issues at some point.

Once you leave your day job, you also leave the security of consistent paydays each month. It means you have to be stricter about pulling money out of your business and ensure you have enough to cover bills no matter what date they’re coming out.

If you do client work too, you have to factor in that sometimes they’ll pay late, and you might need to pay bills in the meantime. Having a pot of cash set aside for this (and also any emergency flat tires, doctor’s appointments, or new tumble dryers) is vital so you don’t put yourself in a financial hole.

A great book covering this topic is called The Barefoot Investor by Scott Pape. You could also check out Rich Dad’s Cashflow Quadrant by Robert T. Kiyosaki, which is specifically about business and money.

Tip 4: Separate Bills from Income

If you’ve published a book, are providing a service (or you’re about to), or you have any other form of secondary income, then I implore you to separate out your finances. It’s easy enough to set up another current account. You don’t need a fancy business account when you start, but you do need to separate the business costs from the normal day-to-day cost of living.

Why? Because come the end of the tax year, you’re going to need to go through your spending and income line by line to work out whether you’ve made a loss or a profit. Having it separated from your household bills will make your life an awful lot easier.

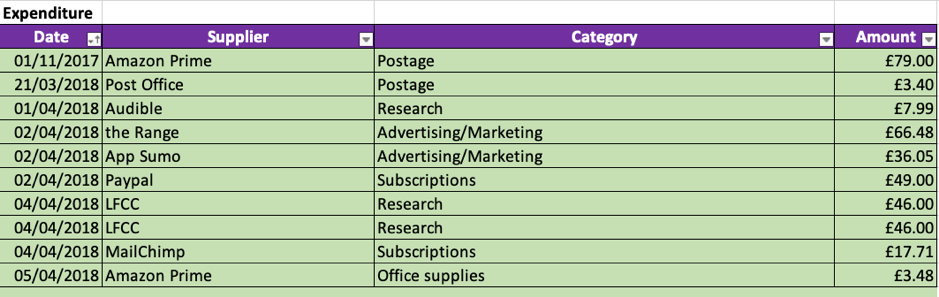

Tip 5: Track it All

We’re words people, not numbers people. But this is one set of numbers we all need to track. If numbers scare you, then keep it simple. All you really need are a few columns in a spreadsheet and a habit of putting in your income and outgoings each month.

I have two spreadsheets, an income one and an expenditure one, though if you’re spreadsheet savvy, I’m sure you could amalgamate them. For your spreadsheets, include these basic columns:

- Income and any explanatory title you want to give it like Amazon sales, Kobo sales, editing work, etc.

- Expenditure, and (again) a description of the type of expenditure, like office furniture, software, or stationery.

- Dates. It’s helpful to keep dates associated with the income or expenditure so you know what tax year it falls into and can find any associated receipts if necessary.

If you’re more technical, consider using a piece of software. There are lots out there that will pull the transactions from your bank into their software and make the accounting and end-of-year tax assessments super simple. I moved to using Xero this year, but there are lots of other options like QuickBooks and Sage. Carefully read the terms and conditions and check for hidden costs.

Tip 6: Have Multiple Income Streams

Lots of writers want to write all day rather than deal with the business or marketing side. And that’s fine, we all have our preferences. What’s dangerous is to leave yourself with only one income stream—e.g. only book sales.

People employed by others generally have more stability than those who are self-employed. But you only have to look at the 2008 financial crash to know that you could be made redundant and lose your income at any time. Which is why, even if you want to write all day, you should protect yourself financially by having other sources of income. If you don’t want to take away from your writing time, then choose passive sources like investments or affiliate income.

Having multiple sources of income will keep your business stable and ensure that no one source has the power to cripple you if it vanished. Some ideas, if you’re confident and have the right skills:

- Editing / critiquing

- Coaching writers

- Formatting

- Organizing writer events etc

- Patreon

You could also think about:

- Investing in the stock market

- Investing in property

- Freelance consulting back into your old career

- Utilizing other skills you might have, like making cakes or sewing, and selling those services

If you only do a few things this year on the business side of your writing, let it be these. Separating out finances and tracking your income and outgoings are the foundations of any business, creative or otherwise. And who knows, 2030 might see you writing full-time.

{kind=link}

19 Comments.

[…] to be a full-time writer? Set up your finances […]

Great advice Sacha! I’m pretty organized in this department thankfully my sorting taxes in preparation for accountant skills have come in handy LOL 🙂

[…] Sacha Black shares 6 steps to setting yourself up financially as a writer in 2020. […]

[…] https://writershelpingwriters.net/2020/01/six-steps-to-setting-yourself-up-financially-as-a-writer-i… […]

Sacha,

Your post came at a perfect time. I’ve been trying to determine if I can totally focus on writing for my career. I’m trying to be realistic, and you’ve given me ideas for how to save up right now and maybe be ready in the next two years.

Thanks so much!

Hi Jackie,

I’m so glad you found it useful. Even though I didn’t want to, I had to set a realistic goal for leaving my job too. You WILL get there. Just keep going on this path 😀

Great advice, Sacha!

Glad you liked it

[…] Source link […]

Great subject.

Thank you 😀

Good article. Thank you, Sacha Black and happy new year.

Thank you and Happy New Year Shoshi 🙂

If I were to leave my day job, my biggest challenge would be finding affordable health care that cover pre-existing conditions. Great topic, Sacha!

Absolutely, it’s definitely a difficult topic and one I can’t talk about personally as I’m in the U.K. and we have a different system here. But I really hope you can find a solution.

I’ve been shocked how much health care has affected my finances, Jill.

It’s scary, trying to figure out the business side of things when you have no experience. The tips here are practical and TRUE—no fluff—providing a primer for anyone needing to figure all this out. Thanks for tackling this topic, Sacha!

It really is. I think quitting my job is the most terrifying thing I’ve ever done, and I’ve given birth! :p Thanks so much for having me and I’m glad you liked it 😀

Thank you for hosting me again, I hope everyone finds this useful. It’s not a topic we like to talk about but it is an important one!